The Compound Cost of Losses: Why Avoiding Drawdowns Matters More Than Chasing Upside

Abstract

Investors are taught to focus on maximizing returns — chasing the next bull run or outperforming a benchmark. Yet decades of financial and behavioral research show that reducing losses is far more important than capturing every gain. Large drawdowns inflict a mathematical and psychological toll that compounds over time, eroding long-term wealth and investor discipline.

This paper explores why losses hurt more than gains help — both mathematically and behaviorally — and why portfolios that prioritize downside protection tend to outperform higher-return, higher-volatility peers over multiple market cycles. Drawing on research from Kahneman and Tversky (1979), Chen (2015), Jondeau et al. (2024), and others, we demonstrate that minimizing drawdowns increases the geometric growth rate of a portfolio, enhances risk-adjusted performance, and improves investor outcomes.

1. Introduction: The Asymmetry of Gains and Losses

The math of compounding is inherently asymmetric. A 50% loss requires a 100% gain to recover. A 20% loss requires a 25% rebound. The larger the drawdown, the harder the climb back — and the longer it takes to simply return to even.

While investors intuitively understand this, few internalize how dramatically it shapes long-term outcomes. Most performance metrics — average returns, beta, alpha — obscure the compounding impact of drawdowns. Over decades, what matters is not how much you gain in good years, but how much you preserve during bad ones.

Consider two portfolios:

Despite earning lower average returns, Portfolio B finishes far ahead. The difference is simple: fewer deep losses and more time compounding.

2. Behavioral Finance: Why Losses Hurt More Than Gains Help

The principle originates from Prospect Theory, introduced by Daniel Kahneman and Amos Tversky (1979). They found that individuals weigh losses roughly twice as heavily as equivalent gains — a bias now known as loss aversion.

“The displeasure associated with losing a sum of money is roughly twice as great as the pleasure associated with gaining the same amount.” — Kahneman & Tversky, 1979

Subsequent studies confirmed this behavioral asymmetry in real-world investing. The disposition effect (Odean, 1998) shows investors tend to sell winners too early and hold losers too long. Myopic loss aversion (Benartzi & Thaler, 1995) finds that frequent portfolio evaluation amplifies the pain of short-term losses, leading to poor long-term decisions.

In essence, drawdowns hurt twice:

- Financially, by shrinking compounding capital.

- Psychologically, by triggering panic and causing investors to abandon strategies at the worst times.

Even if a strategy performs well statistically, it fails if investors can’t stay invested. Limiting drawdowns doesn’t just protect portfolios — it protects behavior.

3. The Mathematics of Drawdowns and Compounding

3.1 The Nonlinear Cost of Losses

Portfolio returns compound multiplicatively, not additively. A 20% loss followed by a 25% gain yields zero net progress:

\( (1 - 0.20) \times (1 + 0.25) = 1.00 \)

But a 20% gain followed by a 20% loss leaves you worse off:

\( (1 + 0.20) \times (1 - 0.20) = 0.96 \)

This asymmetry means volatility itself — even when average returns are equal — lowers geometric mean returns. The relationship is defined by:

\( G \approx A - \tfrac{1}{2}\sigma^2 \)

where (G) is the geometric return, (A) is the arithmetic mean return, and (σ) is volatility.

Reducing volatility, especially on the downside, directly raises the compounding rate.

3.2 Drawdown Duration

Drawdown isn’t only depth — it’s time. Research by Dacorogna et al. (2001) shows that prolonged drawdown periods drag down geometric growth even if average returns are unchanged. Time spent “underwater” is time not compounding.

In long-term portfolios, the duration of drawdown can be as damaging as its magnitude.

4. Empirical Evidence: The Long-Term Power of Drawdown Control

4.1 Academic Literature

- Chen (2015), “On Minimizing Drawdown Risks of Lifetime Investments”, demonstrates that minimizing drawdown risk yields higher certainty-equivalent returns for retirement portfolios than optimizing for volatility alone.

- Jondeau et al. (2024), “Large Drawdowns and Long-Term Asset Management”, show that crisis regimes disproportionately affect long-term expected utility; strategies with explicit drawdown control outperform those without, even at equal average returns.

- Grossman & Zhou (1993) introduced the “drawdown-constrained portfolio” framework, showing that imposing a drawdown floor leads to higher expected utility for risk-averse investors.

4.2 Industry Studies

Morgan Stanley’s Drawdowns and Recoveries report (2023) found that across 150 years of market history, every major crash (1929, 2000, 2008, 2020) took 4–6 years to fully recover. Avoiding just the deepest 10% of drawdowns would have increased long-term geometric returns by over 2% annually.

AQR’s Risk Parity and Downside Protection (2019) similarly found that portfolios with explicit downside risk controls (such as volatility targeting or hedging overlays) produced higher Sharpe and Sortino ratios than traditional 60/40 allocations across 50 years of data.

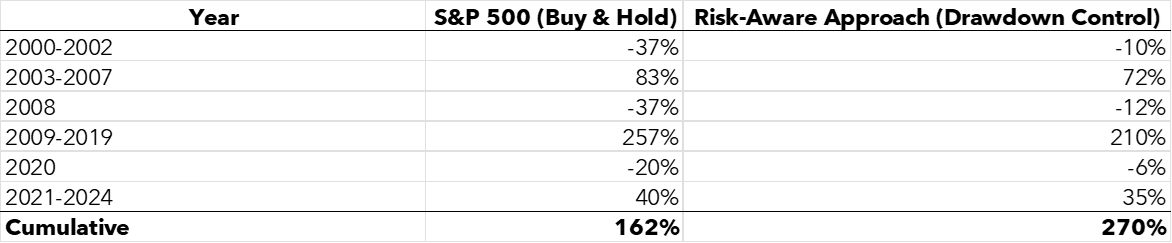

5. Case Study: Compounding Through Two Portfolios

To illustrate, consider two hypothetical investors starting in 2000 with $100,000 each:

Even though the drawdown-aware approach slightly lags in strong years, avoiding deep losses produces a much higher ending value — a direct demonstration of compounding efficiency.

6. Behavioral Advantage: Staying Invested

Most investors don’t lose because markets fall — they lose because they quit. DALBAR’s Quantitative Analysis of Investor Behavior (QAIB) shows that the average equity investor underperformed the S&P 500 by over 3% annually for the last 30 years, largely due to emotional reactions to volatility.

By smoothing returns and limiting pain points, drawdown-aware strategies make it easier for investors to stay the course. That behavioral stability is itself alpha.

7. Risk Metrics That Matter: Sharpe vs. Sortino

Traditional metrics like the Sharpe ratio treat upside and downside volatility equally. Yet investors don’t mind upside surprises. The Sortino ratio corrects this by measuring returns relative to downside deviation only.

\( Sortino = \frac{R_p - R_f}{\sigma_{downside}} \)

In real data, strategies with drawdown control — such as alphaAI’s live leveraged ETF models — exhibit Sortino ratios more than 2× higher than the S&P 500 since November 2024.

This demonstrates not just better returns per unit of total risk, but specifically better returns per unit of downside risk — exactly the type of asymmetry that supports long-term compounding.

8. Implications for Portfolio Construction

- Downside protection improves compounding — reducing volatility drag boosts geometric returns.

- Drawdown control enhances behavioral adherence — smoother equity curves keep investors invested.

- Risk budgeting should focus on downside deviation, not just total volatility.

- Dynamic hedging and risk overlays — using tools like inverse ETFs (e.g., SQQQ) or volatility triggers — can achieve protection without wholesale liquidation (and without capital gains tax events).

- Core and Satellite Allocation — drawdown-aware strategies are ideal for the core of a portfolio, while risk-tolerant, high-volatility strategies can serve as satellites for “play capital.”

9. Limitations and Caveats

While the data favor drawdown mitigation, no method eliminates risk. Hedges can fail, costs may erode gains in low-volatility periods, and regime signals can misfire.

Moreover, each investor’s tolerance and time horizon differ — a retiree prioritizes stability, while a younger investor may accept deeper losses for higher growth potential.

The goal is not to avoid risk entirely but to optimize it — minimizing the type of risk that permanently impairs compounding.

10. Conclusion

The evidence is clear: in long-term investing, the path matters as much as the destination.

Avoiding the market’s deepest drawdowns — even at the expense of missing some upside — leads to stronger compounding, higher risk-adjusted returns, and greater investor confidence.

Losses hurt more than gains help — not just psychologically, but mathematically. The smartest way to build wealth isn’t to chase every rally, but to survive every crash.

At alphaAI Capital, these principles are the foundation of our Risk-Aware Buy & Hold strategy. We believe the core of every investor’s portfolio should be built around disciplined compounding — not speculation or prediction. That means staying invested in the market’s long-term growth engine while introducing intelligent, rules-based hedging that aims to reduce deep drawdowns.

Our approach keeps clients fully invested in broad equities, while dynamically introducing protective exposure (such as inverse ETFs like SQQQ) during high-risk periods. Importantly, this happens without selling core holdings, preserving both tax efficiency and long-term compounding.

The result is a modern evolution of buy-and-hold — one that maintains simplicity and transparency, but integrates institutional-grade risk management. By focusing on what truly drives wealth creation — minimizing drawdowns, preserving capital, and keeping clients invested through full market cycles — alphaAI Capital seeks to help investors achieve smoother, more resilient growth over decades.

References

- Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica.

- Odean, T. (1998). Are Investors Reluctant to Realize Their Losses? Journal of Finance.

- Benartzi, S., & Thaler, R. (1995). Myopic Loss Aversion and the Equity Premium Puzzle. Quarterly Journal of Economics.

- Chen, A. (2015). On Minimizing Drawdown Risks of Lifetime Investments. Insurance: Mathematics and Economics.

- Jondeau, E., Rockinger, M., & Zhang, B. (2024). Large Drawdowns and Long-Term Asset Management. Journal of Risk and Financial Management.

- Grossman, S., & Zhou, Z. (1993). Optimal Investment Strategies for Controlling Drawdowns. Mathematical Finance.

- Dacorogna, M. et al. (2001). Effective Return, Risk Aversion and Drawdowns. Physica A.

- Morgan Stanley (2023). Drawdowns and Recoveries: Lessons from 150 Years of Market History.

- AQR Capital (2019). Risk Parity and Downside Protection.

- DALBAR (2024). Quantitative Analysis of Investor Behavior.

Supercharge your trading strategy with alphaAI.

Discover the power of AI-driven trading algorithms and take your investments to the next level.

Continue Learning

Dive deeper into the world of investing and artificial intelligence to unlock new opportunities and enhance your financial acumen.

Paul Merriman’s Ultimate Buy & Hold Portfolio: Historical Review and Modern Risk Considerations

.jpg)

How AI Safely Manages Leveraged ETFs for Long-Term Investors

The Compound Cost of Losses: Why Avoiding Drawdowns Matters More Than Chasing Upside